Perhaps this aggressive proposal by Germany is one of the unintended consequences of the ECB’s three year long term refinancing operation (LTRO). If eurozone banks have as much access to cheap, three-year ECB funding as their collateral allows, perhaps Germany and the troika have decided that eurozone banks can survive a Greek default.

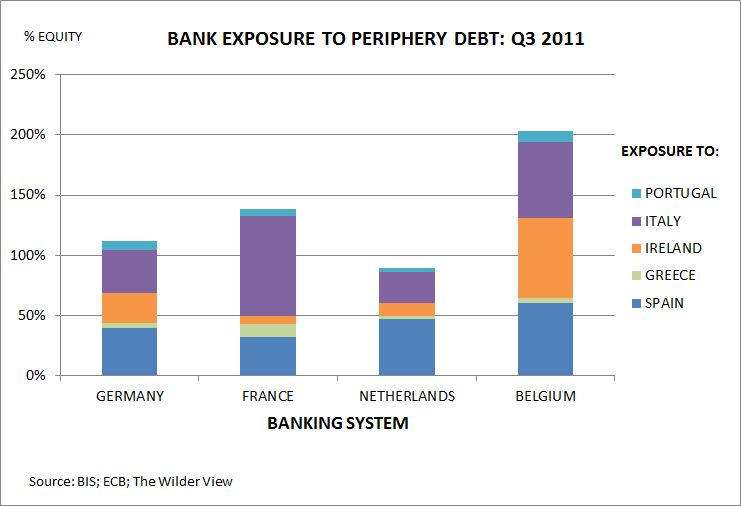

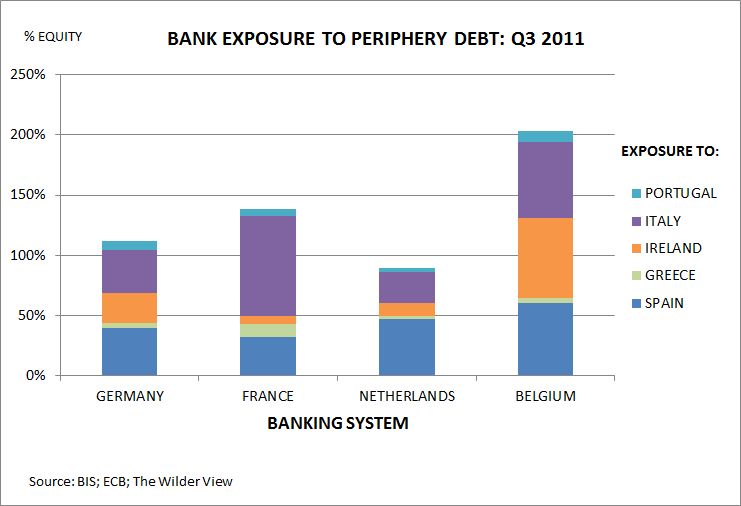

Perhaps naively so, I look at the BIS statistics and see quite clearly that the Germans and the troika would be wrong as regards the Eurozone banks being able to sustain contagion effects of a Greek default and/or exit. Exposure levels remain too high as a share of equity.

Better put: if I look at key core bank exposure, German, French, Dutch, and Belgian, to the Periphery economies as a share of total equity, these banks could go bankrupt if a Greek exit/default spreads to broad Periphery exposure.

Belgian banks especially are in the the red, with total periphery exposure being valued at just over 2X equity. This means that if the Belgian banks were jointly forced to write down all periphery holdings to 49% of what they are holding on their books – according to the IMF 39% of European banks hold their sovereign exposure to maturity, where sovereign exposure is a subset of the BIS data above – their equity would be completely wiped out and technically insolvent. French and German banks are in slightly better shape, but still exposed at holdings of 1.4X and 1.1X equity, respectively.

Banks have improved solvency ratios, as Q3 2010 periphery holdings as a % of equity were higher:

Germany 166%

France 202%

Netherlands 120%

Belgium 291%

Unless the German, French, Dutch, and Belgian governments are planning to inject equity into their banking systems – they haven’t announced such a grand plan to date – banks remain overly exposed to periphery asset valuations. Thus, I can only conclude the following: the Germans and the troika either (1) have a plan to quickly recapitalize the banks across Europe, or (2) could be making a huge mistake.

Source data: BIS, table 9D; ECB for total equity; and ECB for FX conversion.