The growth and fiscal policy adjustments assumed under the program individually have precedent in other countries’ experience, but experience to date under the program suggests that Greece will not be able to set a new precedent by realizing at the same time and from very weak initial conditions a large internal devaluation, fiscal adjustment, and privatization program.

Rob Parenteau and Marshall Auerback sum up the implications of this point (1 A.):

On the first page of the document is not only a pretty open and blatant admission that expansionary fiscal consolidation (EFC) has proven to be a contradiction in terms, at least in Greece, but there is also a serious policy incompatibility problem, at least over the intermediate term horizon, with efforts at internal devaluation (ID) – that is, attempting nominal domestic private income deflation in order to improve trade prospects when one has a fixed exchange rate constraint.

I agree with Rob and Marshall – the grand plan does not work. Greece will (of course) not be able to set a new precedent of public sector and private sector deleveraging amid weakening external demand and a fixed exchange rate. However, I’d like to focus here on the ‘precedent in other countries’ experience’. What precedent?

One might point to Canada’s mid-1990s budget initiative that dropped program spending from 16.8% of GDP in 1993-1994 to 12.1% in 1999-2000 as a candidate for precedent. Marshall Auerback and Stephen Gordon refuted this claim as applicable to current conditions. However, we now have economic data available with which to compare the Canadian austerity experience to that of the Euro area.

What’s happened in Europe over the last year: Divergence. Since the middle of 2010, fiscal austerity and a drive for internal devaluation to ‘increase competitiveness (whatever that is) slashed GDP growth on a quarterly basis for all countries under the European Financial Stability Facility (EFSF) program – Greece, Ireland, and Portugal – while nonprogram countries enjoyed the economic benefits associated with a robust global recovery (through 2010). Note: fiscal austerity and ‘reform’ are pre-conditions to accessing funding at the EFSF. Not coincidentally, since Q1 2010, no Euro area countries have contracted except program countries (rounding to the nearest tenth) through Q2 2011.

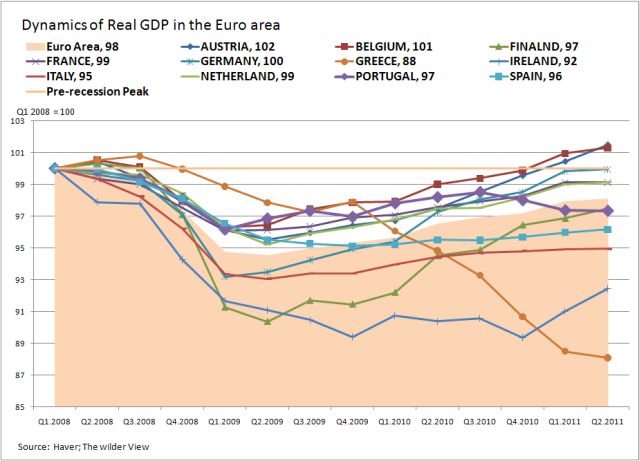

The chart above illustrates the major Euro area (EA) economic (EA 12 less Luxembourg) recoveries since the peak in EA real GDP, Q1 2008. The legend lists the latest Q2 2011 reading as an index to the Q1 2008 EA peak – the difference over 100 represents the accumulated growth in real GDP. Only Belgium, Austria, and Germany retraced, or fully recovered, the lost EA real GDP. EA economic activity is 2% below pre-recession levels. Notably, Ireland, Greece, and Portugal are struggling amid tight financial conditions and the crimping of domestic demand (internal devaluation).

Since austerity and raising the primary balance is a condition for EFSF funding access, a contracting economy is to be expected, right?

Wrong – in fact, the Canadian economy experienced no real GDP contraction spanning the years 1994-2000 when the structural fiscal balance turned from a 6.9% deficit to a 1.5% surplus. All the while, GDP maintained a 4% average annual growth rate and did not contract on a quarterly basis (after revisions). Admittedly, the Canadian economy did not grow in Q2 1995 and Q3 1995, but improved smartly thereafter.

I point you again to Marshall Auerback and Stephen Gordon for the whys. But basically, easy monetary policy, depreciation of the currency, and robust US demand fostered the fiscal shift in Canada. None of these conditions exist in the Euro area, so those program (austerity) countries – Ireland, Greece, and Portugal – suffer contraction.

As an aside, some may point to Ireland as a success story, since it posted two consecutive quarters of reasonably strong growth in the first half of 2011. Sure, Ireland eventually grew – it is a very open economy, so has an innate ability to generate net export income. But importantly, look how far the economy fell (see first chart). The economy saw 10.7% in accumulated contraction spanning Q1 2008 to Q4 2010 – the 3.5% rebound spanning the first half of 2011 pales in magnitude. I point you to Edward Hugh’s commentary for a sobering read on Ireland.

Finally, I leave you with a potent illustration of what not to do when it comes to fiscal austerity: Portugal vs. France.

Portugal was doing all right – better than France, even – until they ran into 2010 financial stability problems that forced the government to start ‘cutting’. Portugal started to contract in Q4 2010, applied for funding in April 2011, and contracted thereafter. Economic Intelligence Unit sees Portugal contracting throughout 2012 (no link). The Euro area prescription for austerity is tantamount to economic collapse amid a fixed exchange rate and meager global growth prospects.

The EA policy plan for fiscal austerity is setting a precedent, all right, a precedent for policy failure.