Last week Jake Tapper, host of CNN’s “State of the Union,” interviewed Trump on a wide range of issues. It wasn’t long before the conversation turned to trade, jobs, and China. “You have to take the jobs back from China” before you can even begin to solve problems like the national debt and healthcare, Trump asserted.

Tapper slyly pointed to a Trump necktie he had put on for the occasion. “Isn’t it hypocritical of you to talk about this,” he asked, “while you’re manufacturing your clothes in China?”

“Not at all,” Trump replied. “A lot of them are made in China, because they’ve manipulated their currency to such a point that it’s impossible for our companies to compete with them.”

So, does China really manipulate its currency? Can we blame China for the lack of American competitiveness? We’re going to hear a lot about Chinese currency manipulation before this presidential campaign is over, so it might be a good idea to do some fact checking right at the outset.

Yes, China is a “currency manipulator” in the narrowly technical sense that it uses monetary policy to influence its exchange rate. According to the IMF, so do more than half of the other countries in the world—friendly countries both rich and poor like Switzerland, Bulgaria, Costa Rica, Kenya and dozens of others. Having a fixed exchange rate, or one that is allowed to float only within a managed range, is entirely consistent with the agreed rules of international trade.

When politicians call China a currency manipulator, though, they have something else in mind. They claim that China consistently holds the yuan so far below its fair market value that even the best managed American companies could not compete if they tried.

A few years ago, in the immediate aftermath of the global economic crisis, that charge did have a degree of credibility. China had abandoned its previous policy of allowing its currency to appreciate gradually against the dollar and returned to a fixed exchange rate. By early 2010, US economists were estimating that the yuan was 20 to 40 percent undervalued—a margin wide enough to have a significant effect on the competitiveness of US exports.

However, Trump and others who still make the charge of currency manipulation have not been watching the numbers over the past five years—or if they have, they are hoping their listeners have not. Since June 2010, the yuan has once again been steadily gaining in value.

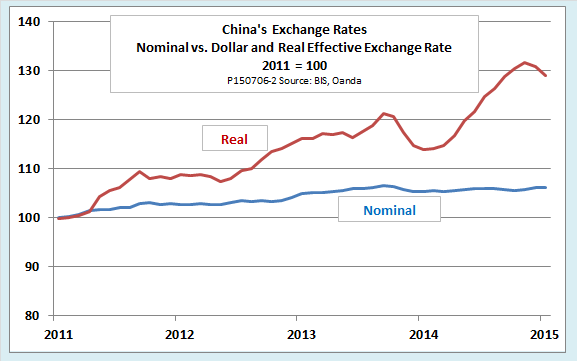

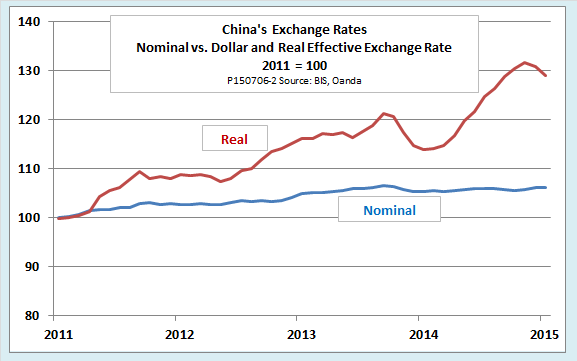

True, in nominal terms, as measured against the dollar alone, the appreciation has been modest, only about 6 percent over five years. The nominal yuan-dollar rate doesn’t tell us much, however. What counts for competitiveness is the real effective exchange rate. That rate differs from the nominal yuan-dollar rate in two ways: First, it takes into account the currencies of all of China’s trading partners—the EU, which is the single largest, countries like Brazil and Australia, which supply its natural resources, and all the rest, including, of course, the United States. Second, the real effective exchange rate takes inflation into account. Inflation has been pushing Chinese wages rapidly higher relative to those in the United States and other Western countries. Inflation, it turns out, has had a much bigger impact on competitiveness than movements in nominal exchange rates. (For more on real vs. nominal exchange rates, see this slideshow.)

The following chart gives the numbers. In contrast to the modest rise in the nominal yuan-dollar rate, China’s real effective exchange rate has soared 30 percent over just the last four years. The supposed 20 to 40 percent undervaluation is a thing of the past.

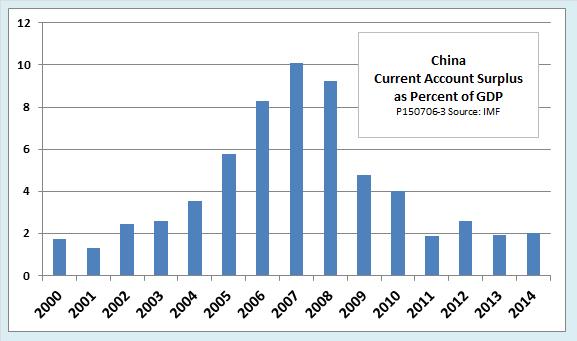

Not surprisingly, as China’s currency has appreciated, its once-phenomenal trade surpluses have dwindled. The next chart shows that the current account balance, the broadest measure of those surpluses, has fallen to just a fifth of its level before the global crisis.

But here is an even more curious development—one that really undercuts the accusations of Trump and others. Although the Chinese government does continue to intervene in foreign exchange markets, it has recently devoted its efforts to boosting the value of its currency, not to holding it down. It does so by selling off foreign exchange reserves in order to mop up what it sees as an excess supply of yuan. The Wall Street Journal reports that in the first three months of the year, China’s foreign exchange reserves fell by more than $100 billion—a record for a single calendar quarter. The government is, of course, aware that a strong yuan, combined with rising Chinese wages, is eroding its once fearsome competitiveness, but it apparently has an even greater fear: A falling yuan might provoke massive capital outflows that could further slow the growth of GDP.

The bottom line: Donald Trump, not China, is the manipulator—a manipulator of the truth.

Related posts:

Real and Nominal Exchange Rates: A Tutorial

Who are the Biggest Trans-Pacific Currency Manipulators?