That’s what macroeconomists are trained to do. Without our meddling, the economy wouldn’t perform very well. Indeed, it would fall into recessions on a regular basis, and might never come out without our help. You see, we are superheroes. Like the Hulk, we are scientists with amazing powers to lift an entire economy out of a ditch and back on the road to prosperity. Our professors taught us how to use very sophisticated mathematical models to design just the right mix of fiscal and monetary policies to manage the economy.

I wasn’t at Yale quite when Yardini was, but I don’t think we missed by much. What he says pretty much coincides with what I remember from being there in the late 1960s. We were taught the art of meddling, that’s for sure, although I remember the favored term as “fine-tuning.” The economy was not so much a car in the ditch as a balky TV that needed its rabbit ears tweaked by a well-trained expert.

Among the superheroes of that time were Gardner Ackley, Otto Eckstein, and Arthur Okun, three of the most distinguished economists ever to sit on the Council of Economic Advisers. In their 1966 Economic Report to the President, they wrote

It is now within our capabilities to set more ambitious goals. . . We strive to avoid recurrent recessions, to keep unemployment far below rates of the past decade, to maintain price stability at full employment . . . and indeed to make full prosperity the normal state of the American economy. It is a tribute to our success . . . that we now have not only the economic understanding but also the will and determination to use economic policy as an effective tool for progress.

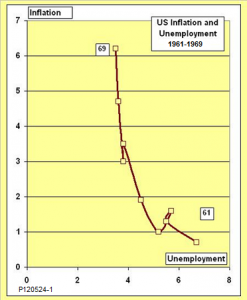

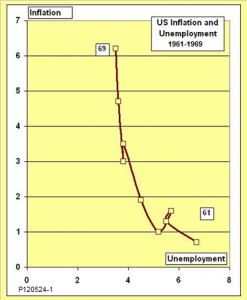

So, how did it work out, all that masterful fine-tuning? Pretty well, at least at first. This chart shows what unemployment and inflation looked like in the Kennedy-Johnson years. It looks a lot like a Phillips curve, doesn’t it? Twist those knobs labeled fiscal policy and monetary policy, and you can choose just the point on the policy menu that you prefer. If you would like to accept a little more inflation, that’s fine, and you’ll get a nice reduction in unemployment in return.

Toward the end of the 1960s, however, things started to go wrong—things that were never mentioned in our macroeconomics class, or, if mentioned at all, were glossed over with wave of the hand.

First, there were policy lags. We learned that there were lags in IS-LM model, of course, but only as a concept; no calendar time was ever given for them. We would have been astonished to learn that the response time after turning the monetary and fiscal policy knobs was on the order of two full years for real GDP and longer than that for the price level.

Then there were forecasting errors. Computers were in their infancy. The one I ran my dissertation models on occupied a room the size of a basketball court and had about the same computing power as my microwave does today, but we were in awe of them. One of the things they did most awesomely was crank out forecasts based on fleshed-out versions of the IS-LM model. We would have sunk into shocked disbelief if we had been told that those forecasts had no greater accuracy than the assumption that next year would be exactly like this year.

Most insidious of all, there was time-inconsistency. I don’t remember ever encountering that concept at Yale. Time-inconsistency is one of those clunky terms economists use to talk about things we are familiar with from everyday life, in this case, the fact that people sometimes pursue short-term objectives that are different from their long-term best interests. The classic case is the decision of whether to have one more drink before you leave the party. Economic stimulus just before an election is equally a classic.

The macroeconomic superheroes of the day were not supposed to be subject to time-inconsistency. Remember, “We now have not only the economic understanding but also the will and determination to use economic policy as an effective tool for progress.” If only.

When you put lags, forecasting errors, and time-inconsistency together, you get something much nastier than a Phillips curve. You get a stop-go cycle with an inflationary bias. You keep the expansion phase going too long, because you don’t want to take the bitter medicine of disinflation until after the next election. Then, like a poorly disciplined patient with drug-resistant tuberculosis, you stop taking your disinflation pills as soon as you feel a little better, but before the cure is complete. The cycle goes around and around. The top of each cycle has a higher rate of inflation than the one before, and the bottom has a higher rate of unemployment. Here is the full chart of how things played out after those early days of seemingly successful meddling in the early 1960s. Taking the 1960s and 1970s as a whole, it looks like the macroeconomists of the day were less the superheroes who lifted the car out of the ditch than the impaired drivers who put it there.

The take-away for 2012? Beware of macroeconomic meddlers. To their credit, the current generation of economic advisers and policymakers—the Larry Summers, the Greg Mankiws, and most of the rest—are well aware of the pitfalls posed by the terrible trinity of lags, forecasting errors, and time-inconsistency. They know that the ideal is to follow preset policy rules, and if they can’t bring themselves to do that, that they should tweak the policy dials only a little at a time and wait cautiously to see what happens. Some of them may score pretty high on the self-esteem scale, but none of them are as recklessly overconfident as the macroeconomic superheroes of the 1960′s appear, in retrospect, to have been. But they are only advisers. Their clients still face the temptation to meddle.

Obama definitely has some of the instincts of a meddler. They are exemplified by his technocratic attempts to fine-tune environmental and energy policy with a CAFE standard here, an electric car subsidy there, and half a pipeline somewhere else. His 2009 stimulus program was somewhat in the spirit of the 1960s, although it ended up doing neither much harm nor much good. Whether you thought it was too much or too little is moot; Republican opposition is likely to preclude any repetition in a second Obama administration, if there is one.

Macroeconomic management under a possible Romney administration is more of a cause for concern. The candidate’s call for a 4 percent unemployment rate—a goal “far below rates of the past decade”—makes me nervous. Getting to that goal, if it is more than just empty campaign rhetoric, would require boosting real GDP well above its long-term potential.

Somehow, the economic meddlers of the day, whether Republican or Democratic, never see a boom for what it is. Instead, they see it as a new normal of endless prosperity, just as the 1966 Council of Economic Advisers did. If the Bush years taught us anything, it is that Republican vows of responsible fiscal policy go out the window under boom conditions. Even if a Romney administration did manage to bring the budget into balance, that would not be enough at the peak of the business cycle. A 4 percent unemployment rate, if such a thing were ever again to come about, would call for a substantial budget surplus plus monetary restraint. Otherwise, we would get more overheating and another crash.

Could we count on a Republican White House backed by a Republic Congress to avoid the siren call of time-inconsistency? Or would we end up with a new boom-and-bust cycle different from, but no less destructive than, that of the 1960s and 1970s?