Tax Deduction or Tax Expenditure?

When economists look at deductions, credits, exclusions, and other tax preferences, they do not see reductions in the burden of government. Instead, they see disguised forms of spending that, at best, leave the burden of government unchanged, and more likely, increase it. That is why they prefer the term “tax expenditure.” A simple example will explain why the term is apt.

Suppose the government decides it is time to replace the aging 747 that serves as Air Force One with a shiny new Boeing Dreamliner. The list price, without the upgrades the president will need, is about $200 million. How to pay for it? The Treasury could write a check for $200 million to the Boeing Company, in which case it would appear in the budget as an ordinary line-item expenditure. Instead, it could compensate Boeing with a $200 million tax credit. Boeing wouldn’t care which. (I am assuming here that Boeing actually pays taxes, as it claims to do; a premise that some dispute.) People who worry about the burden of government should not care much, either. Whichever way the government pays for the Dreamliner—writing a check or making a tax expenditure—the purchase places a $200 million burden on the public. The burden must take one of three forms, or a combination of them:

- Someone will have to pay $200 million in additional taxes

- Some other expenditure will have to be cut by $200 million

- The government will have to borrow the funds, which means $200 million in future tax increases or expenditure cuts (unless the Treasury intends to default, a possibility we won’t consider here).

Does this reasoning mean that we should classify all tax cuts as tax expenditures? No. It is true that the government would have to resort to one of the three alternatives listed above if it announced a simple tax cut of $200 million, but there is an important difference. A tax cut unconditionally leaves money in the pockets of citizens that they can use to buy something they themselves want. A tax expenditure imposes a condition that citizens spend the money they would otherwise have paid in taxes on something the government wants. The attached conditions that direct spending into certain areas are what makes the charitable deduction a tax expenditure.

Are Tax Expenditures Ever a Good Idea?

Tax expenditures need not always be a worse way for the government to buy what it wants than direct, on-budget spending. There are at least two reasons they could sometimes be better.

One is the possibility that tax expenditures may allow greater consumer choice. For example, suppose the government, worried about climate change, wants to encourage home energy efficiency. A tax credit for replacement windows, insulation upgrades, or replacing appliances would allow homeowners to choose the kind of investment that gave the greatest payoff for their particular home. For a given impact on the budget, it might well be more efficient than, say, hiring government crews to go from home to home to install insulation upgrades. (Note, however, that a carbon tax or some other form of energy signal would arguably be better than either approach.)

A second possibility is that a tax expenditure might induce people to purchase some public good from private suppliers that operate more efficiently than a government agency. For example, if private health insurance companies operated more efficiently than government programs like Medicare, it could make sense to expand health care coverage using tax credits instead of by broadening Medicare eligibility. (Again the example is hypothetical. In practice, it is far from clear that private insurers are more efficient than Medicare administrators.)

Imperfect though they are, these examples show that we should not rule out tax expenditures as a way to encourage the supply of desirable public goods. However, they also remind us that the real test is whether a given tax expenditure encourages the purchase of goods or services that are really worth their cost in terms of public funds. If they are not, then considerations of the relative efficiency of tax expenditures and direct expenditures are beside the point.

What Does the Charitable Tax Expenditure Buy?

The question at hand, then, is, What does the charitable deduction really buy? Much less by way of charity than is often thought, at least if we understand charity in the ordinary way.

Charity, to cite a few random on-line dictionary definitions, means “generosity and helpfulness especially toward the needy or suffering,” “provision of help or relief to the poor,” or “generous actions or donations to aid the poor, ill, or helpless.” How do these definitions compare with the actual patterns of giving under the so-called charitable deduction?

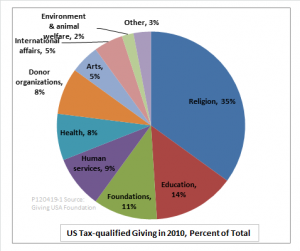

The Giving USA Foundation provides an annual tally of tax-qualified giving. Using IRS data, the foundation estimated 2010 giving at $291 billion. This chart shows a breakdown by category of recipient:

The next question is, What percentage of tax-qualified giving can we reasonably call “charitable,” using the ordinary meaning of the term? Clearly not all of it.

Let’s begin with the largest category, religious giving. Many people think of support for churches as the essence of charity, and spokespeople for the sector do their best to reinforce that view. For example, writing on the website breakpoint.com, Chuck Colson tells us that “charities, especially religious charities, provide services that the government won’t or can’t do efficiently. . . Look just at what Catholic Charities does for AIDS victims, or for the savings religious schools provide municipalities. Or the services provided by homeless shelters, prison ministries (like Prison Fellowship), medical research, and on and on.”

If we look past the rhetoric at the actual numbers, though, we get a different picture. The next chart shows some useful data from a survey of church budget priorities provided by Christianity Today.

What we see is that churches spend the most of their budgets on staff and facilities that have worship as their main purpose. Worship is all well and good, but it is not charity. In saying that, we do not have to adopt the cynical attitude of a Samuel Butler, who, in his utopian novel Erewhon, lampooned churches as “musical banks,” where parishioners made deposits but never withdrawals. Even if we accept Christian or other theologies at face value, the purpose of worship is to put the participant at rights with God; it is in that sense an essentially self-regarding rather than a charitable activity.

The truly charitable activities in the Christianity Today breakdown fall under the categories of ministries and missions. Those comprise everything from prison ministries, to soup kitchens, to aid for hospitals in Africa. What we conclude is that charitable activities of religious organizations make up not 35 percent of all tax-qualified giving, but rather, something like 17 percent of 35 percent, or about 7 percent of the total.

Sufficiently diligent research could no doubt track down similar data for the charitable and non-charitable components of other giving categories, but I will, instead, resort to guesswork. The next largest giving category is education. Reasonably construed, the charitable component of giving to education would be the part that provides scholarships for needy students and pupils. Giving money to send your local school’s volleyball team to the state tournament wouldn’t count. Giving money to build a new science building at your alma mater would count only to the extent that students on needs-based scholarship used it, and so on. I am guessing that 20 percent of educational giving might qualify as charitable.

I have equal reservations about the activities of foundations. Foundations support many causes, not all of which are charitable. Not only do they provide many services to people who are not needy; everyone knows that the not-for-profit world is full or organizations that devote 100 percent of their energies to purely political activities. The IRS is notoriously permissive in accepting the slightest fig leaf of educational or scientific purpose to allow partisan organizations to qualify for tax-exempt status.

Much the same reasoning applies to giving for health care. Some of it, certainly, goes to support provision of health care services for the medically indigent, but not all of it. For example, donor-supported medical research results in new treatments that benefit insured as well as uninsured patients. It would be a stretch to suppose that half of this category is truly charitable.

Giving to the arts is very nice, of course, but unless it supports free opera tickets for inner city kids, it is not charity. Much of it caters the personal tastes of wealthy donors, not to the poor and needy.

Suppose we give a pass to donor organizations like United Way, and consider all of their activities to be charitable. Suppose we allow the welfare of animals and endangered plants equal charitable status with the welfare of people. No matter what allowances we make, it is hard to construe much more than a third of tax-qualified giving as truly charitable. Even if you don’t like my guesswork, I challenge you to get that number up to half.

Does the Charitable Deduction Increase Giving?

If the charitable deduction dramatically increased total giving, it might be possible to justify its budgetary cost of $50 to $60 billion per year, even if only a third of the giving were actually charitable in nature. For example, if the charitable tax expenditure generated $3 in new giving for each $1 of cost to the budget, its “charity efficiency” would rise to 100 percent. However, the evidence that the deduction has any effect at all on giving is surprisingly weak.

William C. Randolf of the Treasury department cites several econometric studies in an entry written for the NTA Enclyclopedia of Taxation and Tax Policy. (The entry is available on line here, courtesy of the Tax Policy Center.) He concludes that there is some evidence of a positive effect on giving, but warns that the most recent evidence is not very robust, and offers his opinion that the effect is often overstated.

Neither does historical evidence support the notion that the deduction has much effect on total giving. Writing recently for Nonprofit Quarterly, Jack Shakely examines several episodes in which tax law changes reduced the value of the deduction. One of the first was the 1944 decision to introduce a standard deduction, thereby making itemization unattractive to middle- and lower-income taxpayers. Charities warned that the sky would fall, but the change turned out to have little impact.

The same pattern has repeated itself with every reduction of tax rates for high earners. For example, the Economic Recovery Tax Act of 1981 cut the top rate from 70 percent to 50 percent, almost doubling the out-of-pocket cost of charitable donations to top-bracket taxpayers. Despite forecasts of doom from the nonprofit sector, there was little impact on total donations.

Certainly there is nothing in the empirical evidence to support the idea that a reduction in tax benefits cuts contributions on a dollar-for-dollar basis, as Martin Feldstein claimed in a 2009 editorial for the New York Times. The idea of a “charitable multiplier” greater than one is even farther from reality. Instead, charitable giving has varied surprisingly little over the years, even as top tax rates have risen and fallen dramatically.

The Bottom Line

The bottom line is that the popularity of the charitable deduction rests on a set of false premises. In reality, the deduction is best viewed not as a reduction in taxation but as an increase in expenditures. Surprisingly little of the giving that qualifies for the deduction goes to truly charitable purposes. And warnings that the nonprofit sector would face collapse without the charitable deduction are greatly exaggerated, if not altogether baseless.

My personal conclusion is that Congress should simply abolish the charitable deduction along with the host of other tax loopholes that permeate our rotten tax code. However, that may be too radical for many. For those who cling to the idea that the tax code should in some way encourage charitable giving, I will examine proposals for reform in Part 2 of this post.

Follow this link for Part 2 of this post