President Obama’s 2011 State of the Union Address contained ringing language on corporate tax reform:

Over the years, a parade of lobbyists has rigged the tax code to benefit particular companies and industries. Those with accountants or lawyers to work the system can end up paying no taxes at all. But all the rest are hit with one of the highest corporate tax rates in the world. It makes no sense, and it has to change.

So tonight, I’m asking Democrats and Republicans to simplify the system. Get rid of the loopholes. Level the playing field. And use the savings to lower the corporate tax rate for the first time in 25 years –- without adding to our deficit. It can be done.

That was then. This year, instead, the White House is advocating a handful of minor fiddles that would raise corporate taxes on some while creating new loopholes for others. We won’t get the full details until the February budget message, but here is an outline of what to expect, courtesy of Reuters:

- Eliminating a tax break for moving expenses when a U.S. company ships operations overseas. Replacing it with a tax credit of 20 percent for the expense of moving operations back to the United States. The White House says this is revenue neutral and would not add to the deficit.

- Doubling the domestic production tax incentive for advanced manufacturers to 18 percent, while eliminating it for oil production, to urge manufacturers to create U.S. jobs.

- Closing a tax loophole that allows U.S. companies to shelter profits overseas from intangible property, like royalties from a drug patent. The White House says this would raise $23 billion in revenue.

- Proposing a new credit of $6 billion over three years for investments that help fund projects to improve economic activity in communities hit by major job losses or military base closures. To be done jointly with state economic development agencies.

- Proposing an additional $5 billion in an advanced energy manufacturing tax credit the White House says would leverage nearly $20 billion in U.S. clean energy manufacturing.

- Proposes extending for all of 2012 a provision to allow companies to deduct the full cost of investment in equipment, which the White House says yields $50 billion in tax relief over two years.

Not quite the same, is it? Let’s go back to first principles to see just what is wrong with the corporate tax and why it should be a priority area for tax reform.

The Uncertain Incidence of the Corporate Tax

Who bears the burden of the corporate income tax? Not corporations, which are not people, despite anything the Supreme Court might say. The economic burden of the corporate tax must somehow fall on real people—shareholders, other suppliers of capital, workers, customers, or someone else.

Economists have debated the incidence of the corporate tax for decades. A paper in the Virginia Tax Review, by Rosanne Altshuler, Benjamin H. Harris, and Eric Toder, provides a good summary.

Early work by Arnold Harberger, beginning in the 1960s, concluded that essentially all the burden fell on shareholders. That assumption has become the standard one used when presenting data on the way the overall burden of taxes is distributed among the population. However, Harberger’s analysis applied in full force only to a closed economy. In an open economy, where not just goods and services, but also capital moves easily from one country to another, while labor is less mobile, things are likely to be different.

In today’s open economy, capital flows to countries where corporate tax rates are low. As it does so, the amount of capital invested per worker falls in countries where tax rates are high. Less capital per worker means less productivity and consequently lower wages. In that way, the burden of corporate taxes is shifted to workers. How much of it is hard to tell. Maybe all, maybe 70 percent, maybe half. The shift may vary over time and from one industry to another. In any case, the hypothesis that shareholders bear the full burden of the corporate income tax is increasingly hard to defend.

How much difference does it make? A lot, because the standard assumption that corporate taxes fall entirely on shareholders seriously overstates the amount of taxes paid by high-income groups. For example, consider an estimate published by the Urban Institute-Brookings Tax Policy Center, which uses the standard assumption. The Tax Policy Center estimates that the top-earning 1 percent of taxpayers pay an average of 28 percent of their income in federal taxes, compared to 18.9 percent for the middle 20 percent. However, the 28 percent figure for the top 1 percent includes a corporate tax component of 7.9 percent. What happens if we assume that component falls on labor income, instead of on income to shareholders? Labor income constitutes 93 percent of all income for the middle 20 percent of taxpayers, but just 45 percent for the top 1 percent. It is reasonable to conclude, then, that shifting the assumed incidence of the corporate tax from shareholders to workers would reduce the gap in tax rates between the top 1 percent and the middle 20 percent by at least half. That would mean the U.S. tax system is quite a bit less progressive than the standard data indicate.

Too Many Loopholes

Principles of good tax policy call for a broad base, low rates, and a minimum of preferences, exclusions, and deductions. The U.S. corporate income tax, like the individual income tax, departs widely from the ideal.

Eric Toder of the Tax Policy Center estimates that eliminating corporate tax preferences could potentially save $506 billion over five years. The biggest preferences include deferral of foreign source income of U.S. multinationals, accelerated depreciation of machinery and equipment, a tax credit for low-income housing, and accelerated depreciation of other rental housing. The exact amounts saved are difficult to estimate because of the way different preferences interact and because of possible changes in behavior if tax rates were lower. Toder’s rough estimate is that if Congress closed all loopholes, it could lower the top corporate tax rate from 35 percent to 23 percent without loss of revenue.

Double Taxation of Corporate Profits

One of the most common complaints about the corporate tax is that it hits capital income twice, once when profits are earned by a corporation and again when they are distributed to shareholders. Congress has responded to the problem of double taxation with preferential personal income tax rates on capital gains and dividends, but as I explained in a post last week, that is the wrong approach. Instead of taxing corporate profits at a high rate and then reducing the rate on capital gains and dividends, it would be better to lower the corporate rate and then tax capital gains and dividends as ordinary income. Making such a switch could reduce distortions to business practices without increasing the total tax burden on income from capital.

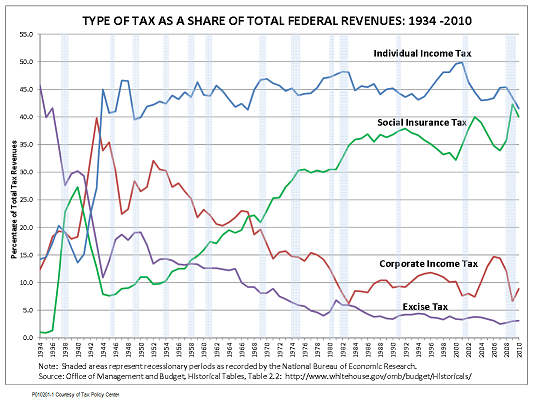

Decreasing Revenue

When Japan reduces its top corporate tax rate this year by 5 percent, as it says it will do, the United States will assume the honor of having the highest corporate tax rate in the world. Yet, despite the sky-high statutory rate and record-high profits, corporate taxes account for a steadily decreasing share of federal revenues. As the following chart shows, corporate taxes now bring in less than 9 percent of federal revenues, down from a post-World War II peak of over 30 percent. Many countries with lower rates bring in more corporate tax revenue as a share of GDP.

In addition to leakages from loopholes, another reason the corporate tax doesn’t bring in much revenue is that most businesses do not pay it. About 7 million businesses file corporate tax returns, but three times that many are not subject to corporate taxes at all. Instead, they are individual proprietorships, partnerships, or subchapter-S corporations. Tax laws allow all of those to pass their profits through to their owners, who then pay taxes on them at individual rates.

Also Read: Faster GDP Growth Will Be Welcome News for the White House, Despite “Ifs” and “Buts” in the Details

What to do?

A case can be made for abolishing the corporate income tax altogether. The government could make up the lost revenue, now less than 10 percent of all federal taxes, in several ways, any of which would produce fewer distortions to business practices than the corporate tax in its current form. Taxing capital gains and dividends as ordinary income would be a good first step. Closing loopholes in individual income taxes would be another. Consumption taxes, like a value added tax or broad-based energy tax, are another possible element of broad tax reform. It would be possible to implement these measures in either in a revenue-neutral manner, or as part of a more comprehensive fiscal consolidation with a mix of spending cuts and revenue enhancements.

Wouldn’t eliminating the corporate tax be regressive? It would not have to be. The paper by Altschuler et al., cited above, estimates that shifting tax liability from the corporate to the individual level, by fully taxing capital gains, would, in itself, be moderately progressive. Remember also that the apparent progressivity of the corporate tax depends on the questionable assumption that shareholders bear its full burden. Finally, the effect on progressivity would depend on what kind of taxes were used to make up the revenue lost from eliminating the corporate tax. Taking all of these points together, we could eliminate the corporate tax in a way that made the system as a whole more progressive, made it less progressive, or left progressivity unchanged.

All discussions of the difficulty of taxing corporate income fairly and effectively comes back to the problem that corporations are not people. Instead, they are more like rats. Scientists say that rats, with their collapsible skeletons, can squeeze through a hole the size of a quarter. Corporations do much the same. With a stroke of a pen, they can morph into a limited partnership or a subchapter-S corporation. They can move their legal residence to an offshore tax haven quicker than you or I could load a U-Haul trailer to move across town. In fact, they don’t even have to move. They can stay right where they are and shift their profits to off-shore subsidiaries using transfer pricing, fees for use of intellectual property, or some other entirely legal gimmick. If corporations are incapable of bearing the economic burden of taxes and can easily evade even the formality of paying them, why tax them in the first place?

If abolishing the corporate tax altogether sounds too radical, the next best thing would be to broaden its base, lower its rates, and close its loopholes, and at the same time, increase individual tax rates on dividends and capital gains. Even modest reforms along those lines could get the U.S. corporate tax down from the highest rate in the world to the OECD average of around 25 percent. Just getting down to the OECD average would remove an important competitive disadvantage for U.S. businesses.

Would it be hard to get this done in an election year? Maybe it would, but that is no reason to take reform off the table altogether, let alone reverse course. Shouldn’t we expect something better in next month’s budget message? It can be done.